Automatic Contributions Mobilize Savings

Organization : Innovations for Poverty Action

Project Overview

Project Summary

A mobile phone-based savings account with an auto-deposit feature allows employees to have a portion of their monthly paycheck automatically deposited into savings.

Impact

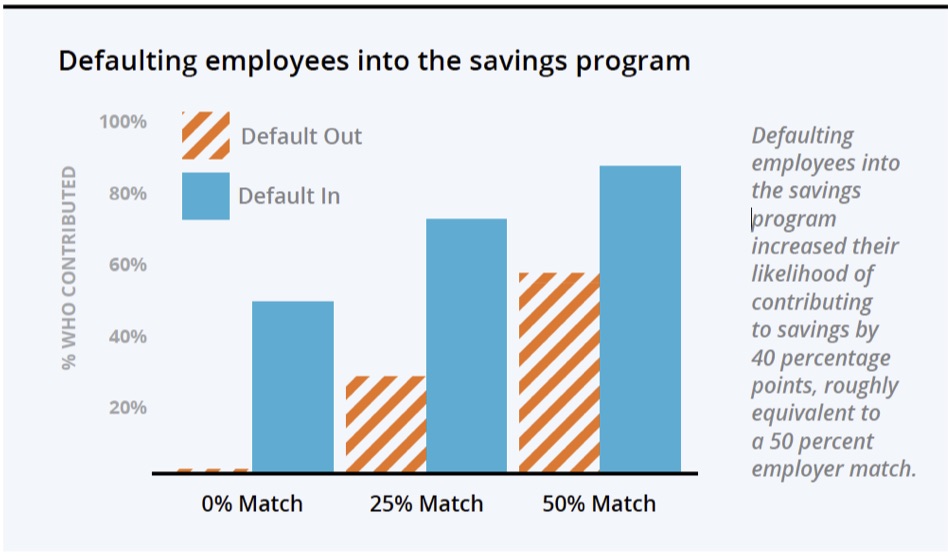

Savings rates increased by 40 percentage points, an effect equivalent to a 50% employer match.

Challenge

Can financial institutions and employers use new mobile money platforms to develop financial products to help individuals in low-income settings reach their savings goals? Research from high-income countries shows that “saving by default,” as happens with 401(k) accounts, can be a very effective way to increase savings, but little has been known about how and whether defaults can help people save in low-income settings.

Design

All Afghan employees at Roshan, Afghanistan’s largest taxpaying corporation, were given a new mobile phone-based savings account called M-Pasandaz. Some employees were enrolled by default, meaning 5% of their salary would be auto-deposited to their M-Pasandaz savings account unless they chose to “opt-out.” Other employees were not automatically enrolled by default; they had to “opt-in” if they wanted to contribute their savings. Essentially, the first group had to deliberately take action if they wanted to stop saving, and the second group had to deliberately take action if they wanted to start saving. All employees were free to change their automatic contribution level to any value between 0% and 10% of their salary.

Consistent with Islamic principles, employee savings accounts did not earn interest. However, as with the common 401(k) account, employees could receive matching contributions from their employer, provided they did not make any withdrawals from their savings account for a six-month period. The amount of matching contribution provided to the employee was either 0%, 25%, or 50%.

Regardless of the amount contributed by the employee to M-Pasandaz, each pay cycle the employees received SMS confirmation of how much had been paid via direct deposit and how much had been placed in the employee’s M-Pasandaz account. Employees were free to check the balance on their accounts and to electronically withdraw money at any time; this was done to enable access to liquidity in times of urgent need. Employees who participated held a broad range of positions at the company, including janitors, security guards, engineers, and managers.

Impact

A randomized evaluation found that employees assigned to “save by default” were 40 percentage points more likely to accumulate savings than employees who had to opt-in to the savings plan, an effect equivalent to providing 50% matching incentives on employee contributions.

Over the six-month study period, those in the default contribution group saved on average an additional 2,426 Afghanis (approximately US$40). Default enrollment also changed employees’ perceptions about savings: these employees reported greater interest in saving and a higher sense of financial security. Even after all incentives were removed and the study had ended, 45%of employees continued to contribute to their accounts.

Participation in the program for those who were neither defaulted into the program nor offered a savings match was only 1%.

What worked best:

- The default combined with the 50% employer match was the most effective, but the default alone proved to be the most cost-effective approach for the employer.

Implementation Guidelines

Inspired to implement this design in your own work? Here are some things to think about before you get started:

- Are the behavioral drivers to the problem you are trying to solve similar to the ones described in the challenge section of this project?

- Is it feasible to adapt the design to address your problem?

- Could there be structural barriers at play that might keep the design from having the desired effect?

- Finally, we encourage you to make sure you monitor, test and take steps to iterate on designs often when either adapting them to a new context or scaling up to make sure they’re effective.

Additionally, consider the following insights from the design’s researchers:

Would this work elsewhere?

- This study contributes to a body of evidence on defaults from high-income countries and suggests that defaults are an effective mechanism to help people save in a wide range of contexts.

- The mobile-based program may work in other countries with high mobile phone saturation and mobile money networks.

Project Credits

Researchers:

Joshua Blumenstock Contact University of California, Berkeley

Michael Callen Harvard Kennedy School

Tarek Ghani Princeton University